How to File Your BIR Taxes as a Filipino Freelancer in 2026 (Complete Step-by-Step)

Hook

You're a Filipino freelancer. Your client paid you ₱120,000 last quarter, your work is mostly invoiced in USD via Wise, and you registered with the BIR as self-employed sometime last year. The April 15 deadline is approaching, you opened the BIR website once, panicked at the form options, and closed the tab.

This guide is the tab you didn't close. We walk through every step: which form applies to your situation, where to download it, how to file it through eBIRForms, where to pay, and which deadlines exist beyond the famous April 15 annual return.

This is informational only. Consult a licensed Philippine CPA for personal tax planning and edge cases. We cite BIR forms and current rates; verify each on the official BIR portal (bir.gov.ph) before filing — regulations can update mid-year.

TL;DR

If you're a self-employed Filipino freelancer earning under ₱3,000,000 a year, you owe the BIR three or four returns per year, not just one:

- 1701Q — quarterly income tax return, due May 15 (Q1), August 15 (Q2), November 15 (Q3)

- 1701A or 1701 — annual income tax return, traditionally due April 15 of the following year (note: BIR extended the 2025 ITR deadline to May 15, 2026 per RMC 30-2026; future years may revert to April 15 — verify each year)

- 2551Q — quarterly percentage tax, due April 25, July 25, October 25, January 25 — only if you elected graduated rates (8% option freelancers are exempt under Section 116 of the Tax Code)

The ₱500 annual registration fee (Form 0605) was abolished in January 2024 under the Ease of Paying Taxes Act (RA 11976). You no longer file it. If anyone still tells you to pay it, they're working off pre-2024 information.

You file most of these through eBIRForms (a free desktop app from BIR) or, less commonly, eFPS (mostly for large taxpayers). Payment is via authorized agent banks, GCash,

Maya, or other BIR ePayment partners.

Late filing triggers a 25% surcharge, 12% annual interest, and a compromise penalty of typically ₱1,000 to ₱25,000 depending on your tax liability. Quarterly returns get skipped most often — don't.

Who needs to file (and which forms apply to you)

Your situation determines which forms you owe. Use this table:

| Your situation | Forms you file annually | Forms you file quarterly |

| Pure freelancer, elected 8% option, ≤ ₱3M income | 1701A | 1701Q |

| Pure freelancer, graduated rates, no VAT registration | 1701A | 1701Q + 2551Q |

| Pure freelancer, VAT-registered (> ₱3M income) | 1701A | 1701Q + 2550M (monthly) or 2550Q |

| Mixed income (employee + freelance), 8% option on freelance side | 1701 | 1701Q |

| Mixed income, graduated on freelance side | 1701 | 1701Q + 2551Q |

The 8% option freelancers have it easiest: one quarterly form (1701Q), one annual (1701A), no percentage tax. That's three filings per year plus the annual ₱500 registration fee.

Graduated-rate freelancers file twice as many forms because the 3% percentage tax (Form 2551Q) is a separate quarterly filing on top of the income tax return.

The single biggest filing mistake we see: people on the 8% option still trying to file 2551Q because they don't realize the option exempts them. Don't. The 8% rate already replaces both income tax AND percentage tax; filing 2551Q on top is double-counting yourself.

The forms, briefly

You don't need to memorize all of these — bookmark this section and come back during filing season.

BIR Form 1701 — Annual Income Tax Return for mixed-income earners (employee salary + self-employment income). Use this if you have a day job AND freelance on the side.

BIR Form 1701A — Annual Income Tax Return for purely self-employed individuals and professionals. Use this if freelancing is your only income source.

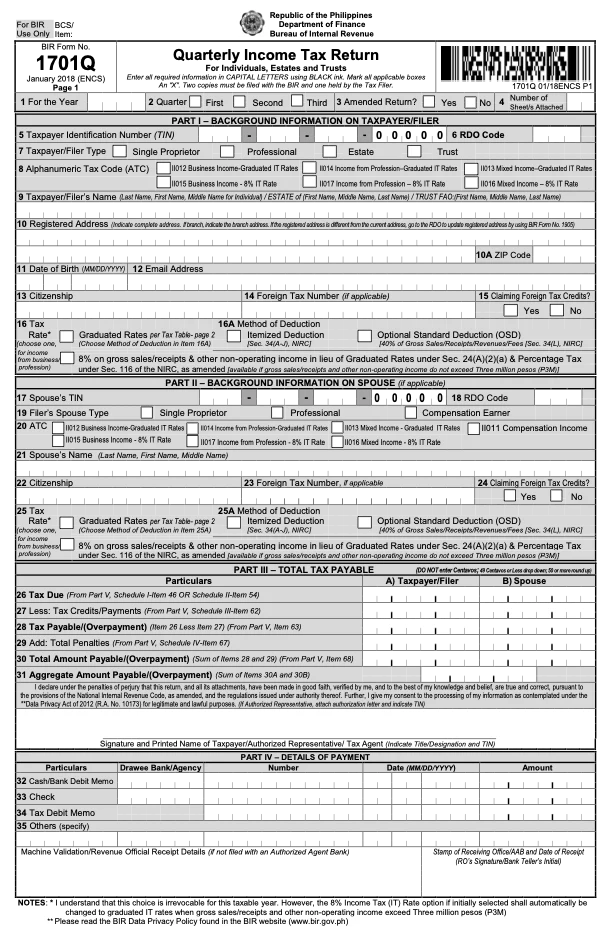

BIR Form 1701Q — Quarterly Income Tax Return. Both 8% and graduated rate filers use this. Three filings per year (Q1, Q2, Q3 — Q4 is rolled into the annual return).

BIR Form 2551Q — Quarterly Percentage Tax. Only filed by graduated-rate freelancers who are not VAT-registered. The 3% percentage tax applies to gross receipts.

BIR Form 0605 — Payment slip for miscellaneous BIR payments (books of accounts renewal, late penalty payments, etc.). Note: The annual ₱500 registration fee that previously required Form 0605 every January 31 was abolished in January 2024 under the Ease of Paying Taxes Act (RA 11976). You no longer file 0605 annually as a routine matter.

BIR Form 2316 — Certificate of Compensation Payment / Tax Withheld. Your employer issues this to you if you have a day job. You attach it to Form 1701 if filing as mixed income.

BIR Form 1905 — Application for Registration Information Update. Use this to change your registered RDO (Revenue District Office), update business name, or formally elect the 8% option if you didn't do it in your Q1 return.

Every form is downloadable as a PDF from the BIR site and fillable inside eBIRForms.

How to file: eBIRForms walkthrough

For 95% of freelancers, eBIRForms is the filing path. It's a free Windows desktop app (Mac users can run it in Parallels or a Windows VM; some freelancers use online filing through the BIR website as an alternative, though the desktop app is more reliable for complex returns).

Step 1: Install eBIRForms

Download the latest version from bir.gov.ph (look for "eBIRForms Package"). Install it on Windows. The app is required because the BIR's portal-based forms occasionally validate XML differently than the desktop version.

Step 2: Set up your profile (one-time)

Inside eBIRForms, enter your TIN, registered name, RDO code, and contact details. This profile auto-fills future returns. If you're not sure of your RDO code, find it on your old BIR registration certificate (Form 2303) or call your registered RDO.

Step 3: Open the correct form

For a quarterly income tax filing, select Form 1701Q from the dropdown. The form opens as a fillable PDF inside the app.

Step 4: Fill in your gross receipts

For 8% filers, this is the simplest part:

- Total gross receipts for the quarter (sum of all client payments)

- The first ₱250,000 of annual gross receipts is exempt — eBIRForms calculates this automatically if you fill in your year-to-date receipts

- The form shows your taxable amount and the 8% tax due

For graduated filers, you'll fill in:

- Total gross receipts

- Total deductible business expenses (with proper documentation in your books)

- Personal exemptions (₱50,000 standard for self-employed)

- The form applies the graduated brackets and outputs your income tax due

Step 5: Save, validate, and generate the XML

Click "Validate" inside eBIRForms. The app checks for math errors and required fields. Fix anything flagged. Then click "Submit" to generate the XML file — this is the official version of your return that BIR processes.

Step 6: Submit and print the confirmation

eBIRForms gives you two submission paths:

- Online submission — the app uploads the XML directly to BIR's portal. You get an email confirmation with a reference number.

- Manual submission — print the form and bring it to your RDO. Slower; use only if online submission fails repeatedly.

Save the email confirmation as PDF. You'll need this if there's ever a discrepancy with BIR records.

Step 7: Pay the tax

eBIRForms only submits the return. You still need to pay what you owe through a separate channel:

- Authorized Agent Banks (AABs) — most

BPI,

BDO,

Metrobank, Landbank, DBP, and

UnionBank branches accept BIR payments. Bring printed Form 0605 (payment slip) along with your check or cash.

- ePayment via GCash — load your GCash, go to "Pay Bills" → "Government" → "BIR," enter your TIN and the form/period. Limit per transaction is ₱100,000.

- ePayment via Maya — similar flow under "Bills." Maya's per-transaction limit is also ₱100,000.

- Landbank Link.BizPortal — pay larger amounts via online banking from any participating bank. No transaction cap.

- DBP PayTax Online — alternative for amounts above the e-wallet limits.

Save the payment confirmation. Late payment penalties apply to the payment date, not the filing date — so even if you file on time but pay a week late, surcharge and interest accrue.

Deadlines: a 12-month calendar

Most freelancers think "tax season = April." It's actually a year-round rhythm. Print this calendar:

| Month | Filing due | What it is |

| January 25 | 2551Q (Q4 prior year) | Quarterly percentage tax for graduated filers |

| April 15 (or as extended) | 1701 or 1701A | Annual income tax return (covers prior year, including Q4). BIR extended the 2025 ITR deadline to May 15, 2026 per RMC 30-2026 — check each year for similar extensions. |

| April 25 | 2551Q (Q1 current year) | Q1 percentage tax for graduated filers |

| May 15 | 1701Q (Q1) | Q1 quarterly income tax |

| July 25 | 2551Q (Q2) | Q2 percentage tax for graduated filers |

| August 15 | 1701Q (Q2) | Q2 quarterly income tax |

| October 25 | 2551Q (Q3) | Q3 percentage tax for graduated filers |

| November 15 | 1701Q (Q3) | Q3 quarterly income tax |

The annual return wraps up Q4 plus reconciles your full-year totals — there is no separate Q4 1701Q. Your Q4 percentage tax (2551Q) is the only quarterly filing due in January of the following year.

The Ease of Paying Taxes Act (RA 11976, January 2024) eliminated the previously-required ₱500 annual registration fee. Don't pay it; don't file Form 0605 for that purpose. Older articles, accountants on auto-pilot, or BIR walk-in staff occasionally still mention this — they're outdated.

If a deadline falls on a weekend or holiday, BIR typically extends to the next business day, but this is at BIR's discretion — don't rely on it. File the prior business day to be safe.

Documents and records you need

Before you file your first return, make sure you have these. Filing without them invites audit issues even if the math is right.

BIR Form 2303 (Certificate of Registration) — issued when you first registered as self-employed. Keep this in a folder you can find in five seconds. It has your TIN, registered business name, RDO code, and tax types.

Books of Accounts — manual ledgers (Cash Receipts Book, Cash Disbursements Book, Journal, General Ledger) that you bought from a BIR-accredited supplier, stamped at your RDO. These are your daily transaction logs. Books expire every five years OR when fully written; you renew by getting a new set stamped and registering them with Form 1905.

Official Receipts and/or Sales Invoices — printed by a BIR-accredited printer under your Authority to Print (ATP). Required: you must issue an OR or SI to every client for every payment received, even if the client is overseas and never asks for one. The ATP is renewable every five years.

Quarterly P&L summaries — you compute these from your books to fill in 1701Q. Most freelancers track these in a spreadsheet.

Client payment proofs — Wise statements, Payoneer payouts, GCash transaction history, bank deposit slips. Keep these for at least 10 years (BIR's standard audit window is 3 years from filing date but can extend to 10 years for fraud cases).

USD income note — if you're paid in USD and convert to PHP via Wise, Payoneer, or remittance, the BIR taxes you on the PHP equivalent at the exchange rate on the date you received the funds, not the day you converted to peso. Wise and Payoneer monthly statements typically include the FX rate; save these.

For more detail on receiving USD from foreign clients, see our guide on receiving international payments in the Philippines.

The mistakes that trigger penalties

These are the patterns we see most often:

1. Skipping quarterly returns. Many freelancers file the annual return but forget Q1, Q2, and Q3. BIR's penalty calculator triggers per missed quarter. By the time you realize at year-end, you owe four times the penalty.

2. Filing at the wrong RDO. If you moved residence or business address and didn't file Form 1905 to update your RDO, the BIR considers your return filed at the wrong jurisdiction. This often results in a "no record of filing" finding during audit. Update via 1905 if you move.

3. No Official Receipts issued. Every client payment requires an OR or SI. Many freelancers think "the client is overseas — they don't need one." BIR's position is that the OR is your records obligation, not the client's. If you can't show OR records for income reported, the deduction validity for graduated filers gets challenged, and 8% filers face scrutiny on gross receipts.

4. Missing the 8% election in the first Q1 return. The 8% option must be elected either in your first 1701Q of the year OR via a separately filed 1905 before your first quarterly return. If you file 1701Q for Q1 without checking the "8% option" box, BIR defaults you to graduated rates for the entire year — and you cannot switch mid-year.

5. Math errors on graduated returns. The graduated bracket calculations are easy to misapply. The bracket determines the rate on income within that bracket, not on total income. Use eBIRForms' auto-compute or a CPA-prepared spreadsheet — don't hand-calculate.

6. Acting on outdated advice about the ₱500 annual registration fee. The Ease of Paying Taxes Act (RA 11976) abolished this in January 2024. If your prior CPA, an older blog post, or a BIR walk-in staff member still tells you to pay it, you don't. Don't waste the ₱500 or the time at the bank.

Penalties: what late filing actually costs

If you file late, BIR charges three things stacked together:

Surcharge (25%) — added to your tax due if filed after the deadline. Example: if you owe ₱20,000 and file late, you owe ₱20,000 + ₱5,000 surcharge = ₱25,000 minimum.

Interest (12% per year) — calculated from the original due date to the date you actually pay. On the same ₱20,000 owed, 30 days late = roughly ₱200 interest.

Compromise penalty — a separate flat penalty for the administrative violation, calculated per BIR's Revenue Memorandum Circulars. Typical range for individual taxpayers: ₱1,000 (small amounts) to ₱25,000 (larger amounts). Use BIR's compromise penalty schedule to estimate.

On a ₱20,000 tax owed and filed 30 days late, your total bill ends up around ₱26,200 — about 31% more than if you'd filed on time. Six months late and you're at roughly ₱28,000-30,000 depending on compromise.

Filing on time but paying late only triggers surcharge + interest (no compromise for the filing itself). Filing late but paying anyway triggers all three.

When to DIY vs hire a CPA

Most Filipino freelancers can DIY their tax filing under the 8% option. The math is straightforward, eBIRForms guides you through the fields, and the quarterly rhythm becomes routine after the first year.

Consider hiring a CPA if any of these apply:

- Mixed income complexity — you have employee salary, freelance income, AND rental or investment income. The interaction between Form 1701 and your employer's 2316 is easy to mis-attribute.

- VAT registration — you've crossed ₱3,000,000 in gross receipts and need to register for VAT. The transition year is full of edge cases.

- Business expense deductions are material to your return — if you're filing graduated rates because of high deductible expenses (rent, equipment, contractors), a CPA's documentation discipline saves you in audits.

- Foreign tax credits — you're a Philippine resident but you've already paid foreign withholding tax on some income. Reclaiming the credit on Form 1701 is non-obvious.

- Audit notice received — if BIR sends you any letter beyond a routine acknowledgment, get professional representation immediately.

For pure 8% freelancers earning ₱300K-₱2M from straightforward client work, the DIY route via eBIRForms is reasonable. CPA fees in Metro Manila for individual freelancer returns run ₱5,000-₱20,000 annually depending on complexity — worth it for peace of mind even when DIY would work.

Your action step

Block a half-day this week. Open eBIRForms (install it if you haven't). Walk through one practice filing using your current year-to-date numbers — don't submit yet, just fill it out to see where you get stuck.

If everything fills cleanly: you're ready for the next real deadline.

If you hit a wall: identify exactly which field tripped you up. That's the question you ask a CPA in a 30-minute paid consultation. Cheaper than a year of CPA fees, gets you unstuck.

The freelancers who pay penalties almost never do so because they didn't know how to file. They do so because they didn't carve out the half-day to learn before the deadline. Carve it.

Disclosure: This article does not include affiliate links. We earn no commission for any tax-related action you take. This is informational only and not a substitute for personalized tax advice from a licensed Philippine CPA. Individual tax situations vary; BIR regulations may update mid-year. Verify current forms, rates, and deadlines on bir.gov.ph before filing.